The Mortgage Cheat Code

How YOU can game the credit money system

The credit/debt fiat money system is broken. If you haven’t been living under a rock, I’m sure you’re aware that something is really messed up in the financial system. Hopefully you’re at least somewhat aware of the reasons why and are placing blame squarely on the structure of the monetary system and not on politics or “capitalism” or “socialism” or corporations or billionaires or any of the other red herrings the bankers desperately hope to distract you with.

If you’re still obsessing over any of those things, that’s okay too, and you’re the reason I started this newsletter. It’s impossible to make good decisions without understanding the relevant information, and when it comes to money, almost no one understands the relevant information. My goal is to change that for as many people as I can reach, to grow the small group of people who are knowledgeable and empowered to make better decisions on money and finance.

Previous articles have been focused on economic theory and how money works at a conceptual level. That’s critically important to understand, and if you haven’t taken the time to read those articles, I know it will open your eyes to the world in a way you’ve never considered before. That understanding will give you a huge advantage in benefiting from what I’m about to describe. But today’s subject is strictly practical, actionable information on one specific financial instrument, and how you can use it to game the broken money system to benefit YOU.

Money Is Not Scarce

If you read my previous articles, you’ll understand that one of the biggest problems with the credit/debt money system is that money is not scarce in this system. In fact, the quantity of money is basically unlimited. That’s because money is created by banks every time they make a loan. Unlike everything you’ve ever thought, banks don’t lend out money that’s given to them by depositors. They create new money, out of thin air, with a computer keystroke, every time they make a new loan. That means in practical terms that the amount of money is only limited by the willingness of banks to make loans. And since banks profit by charging interest to loan out money they can create at zero cost, they’re incentivized to make a LOT of loans.

Now as you can easily see, things that aren’t scarce don’t have a lot of value. The less scarce and more easily available something is, the less valuable it becomes. If you and a friend were standing on the shore of Lake Michigan and you reached down and scooped up a cup full of water, turned to your friend, and said “I’ll trade you this cup of water for your Rolex watch,” he’d look at you like you lost your mind. And rightly so, since a cup of water on the shore of a giant lake is so abundant and easily accessible that it has no value compared to a Rolex watch, which are deliberately produced in very limited amounts to increase their scarcity and value.

The difference between money and the water in that example is that money is not scarce, but it is selectively scarce. If you’re a bank, you have access to as much money as you choose to loan out, at zero cost. On the other hand, if you aren’t a bank, money is only available if the bank decides to create some and loan it to you, or you work hard to earn money someone else already has.

This selective scarcity of money is the root cause of the massive wealth inequality we see today. Money is essential to survive in the modern economy, but access to that money is very unevenly distributed.

So how does this benefit certain people? You might be thinking, but don’t borrowers have to pay the loan back with interest? Of course it’s easy to see how the banks benefit, but plenty of wealthy people are not bankers. And that’s a good point. Here’s how.

Because of the incentives banks have to make loans, the amount of money in circulation tends to keep rising exponentially. The amount of most real goods in the economy, however, typically doesn’t rise as fast. When you have more money circulating in the economy without more goods available, the prices people are willing to pay for those goods will go up. That means prices of some scarce goods rise very consistently over time. Those with access to newly created money in the form of loans benefit by using that money to buy assets that are more scarce than the money they borrowed to buy the asset. So they may buy an asset for $1 million, but by the time the loan is due to be repaid, the continuous inflation caused by the increasing money supply might have pushed the price of that asset up to $1.5 million. So subtract the interest paid from $500,000, and there’s your profit, all for doing nothing but convincing a banker to create some money and let you borrow it. The concept that those closest to the source of new money will benefit the most, because they can buy things before the prices rise, is called the Cantillon effect.

Benefitting from the Cantillon Effect

So how can you benefit? You can see that borrowing a bunch of money and buying a good asset with it would be the perfect way to take advantage of the Cantillon effect. But the problem for most people is, if they go to the bank and ask to borrow a few hundred thousand dollars, they’ll be declined in a millisecond. If you’re not already wealthy, you’re going to have a really tough time getting a big loan at a low interest rate, which is what it takes to make this system work in your favor. Most people only have access to loans in the form of a credit card or personal loan, which will be for a small amount and a very high interest rate. That’s not helpful. Luckily there’s one exception, one way almost anyone can borrow a big chunk of money at a low interest rate, and buy an asset that will increase in price over time as the money supply grows: a mortgage.

If you have the income and credit to support a mortgage payment, it can be a great way to take advantage of the broken monetary system to accumulate some long term wealth. However, there are a few caveats and some simple tricks that can make all the difference.

First, while the constant demand for houses fueled by easy access to newly created money means house prices tend to rise consistently over time, there are no guarantees. The housing market often has periods of boom and bust, and falling prices can last for years. Borrowing is always risky, and you shouldn’t take a risk you don’t understand or aren’t comfortable with. While no one can time the housing market, it’s always good to at least be aware that the housing market does rise and fall in cycles, and try to avoid buying when all signs point to housing being extremely overpriced.

Second, just because houses are rising in price doesn’t mean they’re rising in value. It’s a simple concept, but one most people miss. Like Warren Buffet says, price is what you pay, value is what you get. If you buy a house today for $400,000, and in 10 years that same house sells for $700,000, how much did the value of the house change? The price went up, but the house is still the same house in the same location, it’s just a decade older. And a decade of wear and tear is a decrease in value, not an increase. Think of it this way. You can sell for $700,000 and you have $300,000 of “profit”. But if you want the same house back, you can’t buy it for $400,000 again and pocket the $300,000. You can only get the same house back for the full price you received. You haven’t increased your purchasing power at all in terms of housing with that “profit”. Your house hasn’t become more valuable, your money has just become less valuable when measured against houses. In that sense, you probably can’t increase your purchasing power by buying a house to live in, but you can at least avoid losing purchasing power. If you just save money in the bank to buy a house later, house prices will probably rise faster than you can save. That’s especially true if you’re paying rent at the same time. At least with a mortgage, if you pay long enough you own a house eventually. You can pay rent your whole life and you’ll still own nothing at the end.

Understanding Amortization

The key to making a mortgage work for you is to understand and manipulate the amount of principle and interest you pay over the term of the loan. To do this, you need to understand how a mortgage amortization schedule works. An amortization schedule is basically a big chart of your mortgage payments each month, showing how much of each payment is applied to paying down the principle and how much is paying interest. The payment size is the same each month, but the amount of principle and interest varies over the term of the loan, and that’s key to understanding how to manipulate the system.

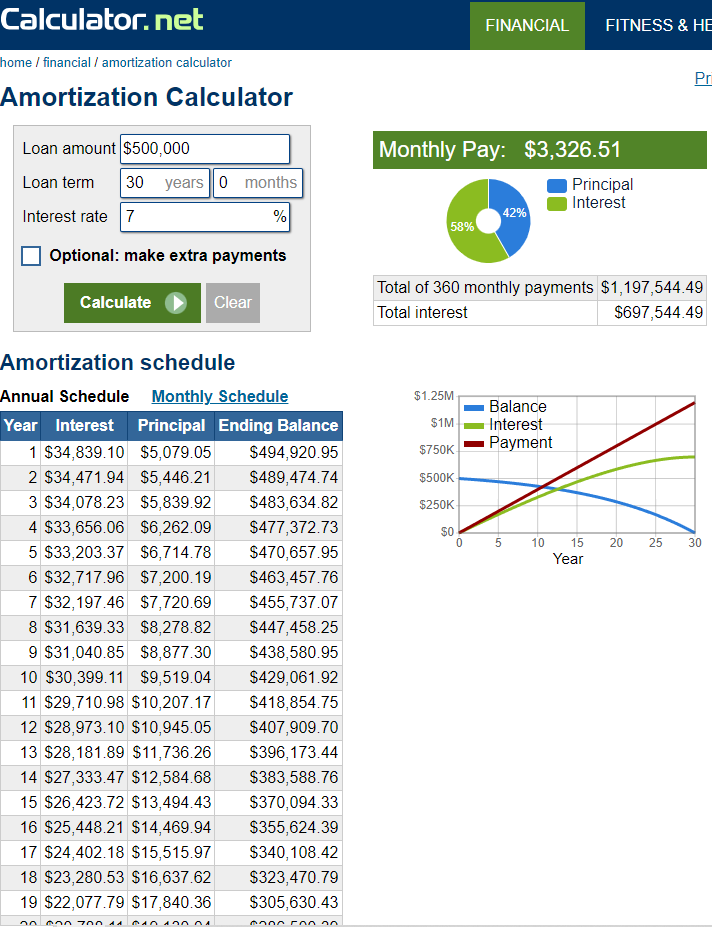

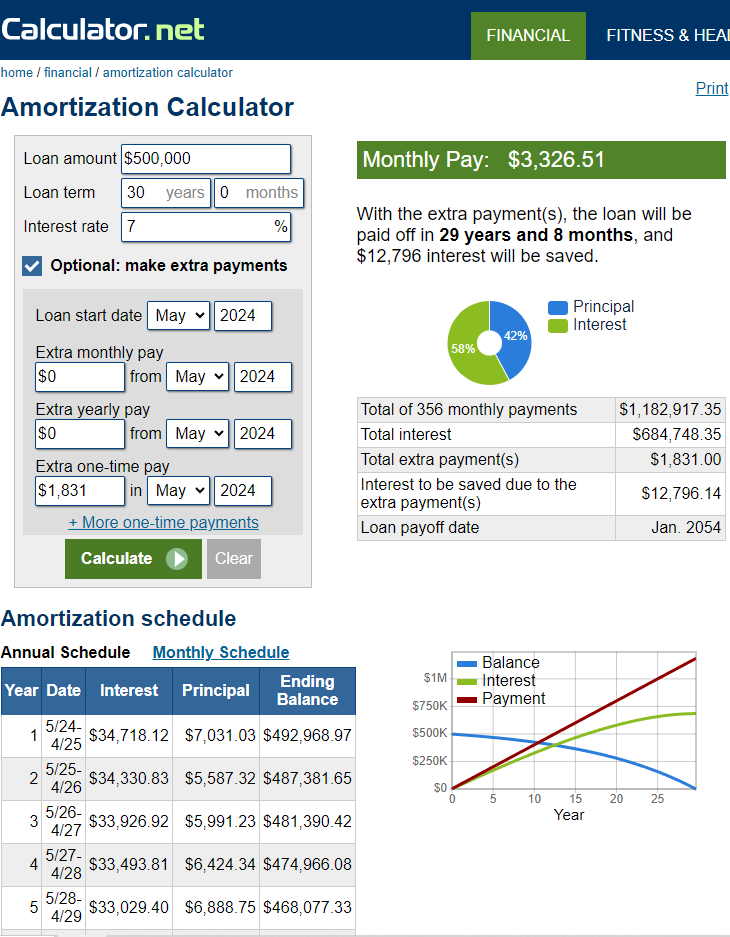

To understand amortization, you need a good amortization calculator. There are plenty of different ones available online, but I’m going to use the one here to illustrate. In this example, I’m going to arbitrarily choose a mortgage size of $500,000 and an interest rate of 7%, but you can of course use your own numbers. When we enter this into the calculator with a loan term of 30 years and click “calculate”, we get something that looks like this.

You can see the monthly payment of $3,326.51, and the total payments over 30 years of almost $1.2 million, almost $700,000 of which is interest. So you end up paying more in interest than the total amount of principle you borrowed. Gulp.

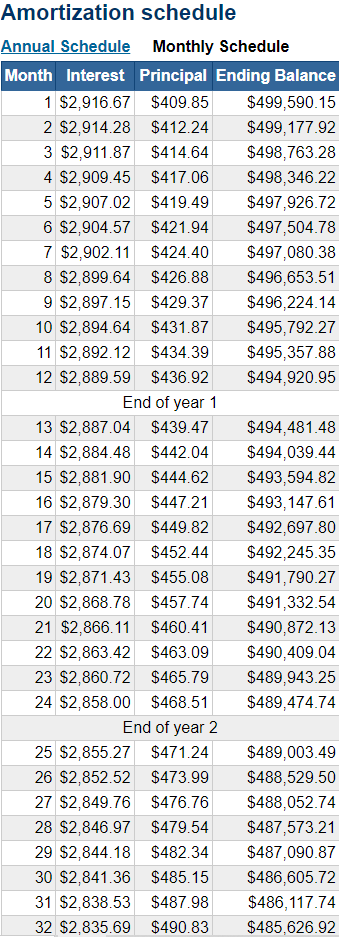

That seems terrible, and it is. But this is where understanding the amortization schedule, that scary looking chart to the left, is going to pay big dividends. First, change the amortization schedule from an annual schedule to a monthly schedule. You’ll see something that looks like this.

So now for each month, you can see how much of the payment is interest, how much is principle, and how much of your original $500,000 balance is still outstanding. As you can see in month one, you’re paying over $2,900 in interest and only $400 in principle, leaving you with a balance of $499,590.15. The reason the interest is so high initially is that you have to pay interest on the full principle balance. As the principle gets paid down, you are now paying interest on a smaller balance. If you scroll down to year 29, you’ll see the opposite situation. In month 338 you’ll pay $2,900 of principle and only $400 of interest. That’s because you’re now paying interest on a balance of only $68,000 instead of $500,000.

As you can see, getting into the later years of the mortgage is a much better situation than paying huge amounts of interest in the first few years. Is there a way to get closer to the end fast? Yes there is, and you may be surprised how easy it is.

Go back to the annual amortization schedule. Suppose you want to take 5 years off your mortgage. How much would it cost to do, and how much would you save in interest? There are two ways to do this, and we’ll cover both.

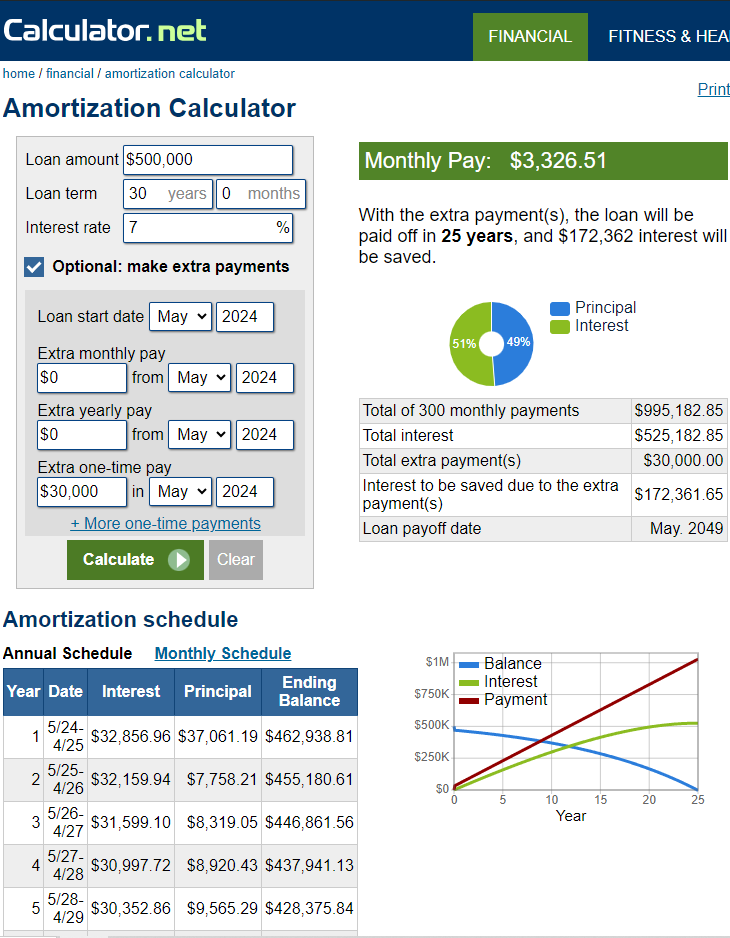

First, the easiest way to get 5 years off your mortgage is to move straight down the amortization schedule to year 6. How can you do that? Look at the annual amortization schedule for year 5. Your ending balance is a little over $470,000. That means to get to that point in the loan repayment schedule, you need to pay $30,000 of principle. So let’s see where a lump sum payment of $30,000 gets us. Inside the box where you entered your loan terms you’ll see a little checkbox labeled “Optional: make extra payments”. Click that box. In the “Extra one-time pay” box, enter $30,000. Click calculate. You’ll see this.

And viola, with the extra payment, the loan will be paid off in 25 years, and you’ll save $172,362 in interest. Pretty amazing results for a one-time $30,000 payment.

Of course for the sake of simplicity, that’s assuming you pay the $30,000 at the very beginning of the loan. Paying the lump sum later into the loan term will change the exact amount of the savings. You can play around with other payment sizes, or even multiple lump sum payments, and see how much each one will save.

But most of you will be thinking, “Where am I going to get $30,000? That’s never going to happen.” If that’s you, don’t worry. We can do the exact same thing a different way.

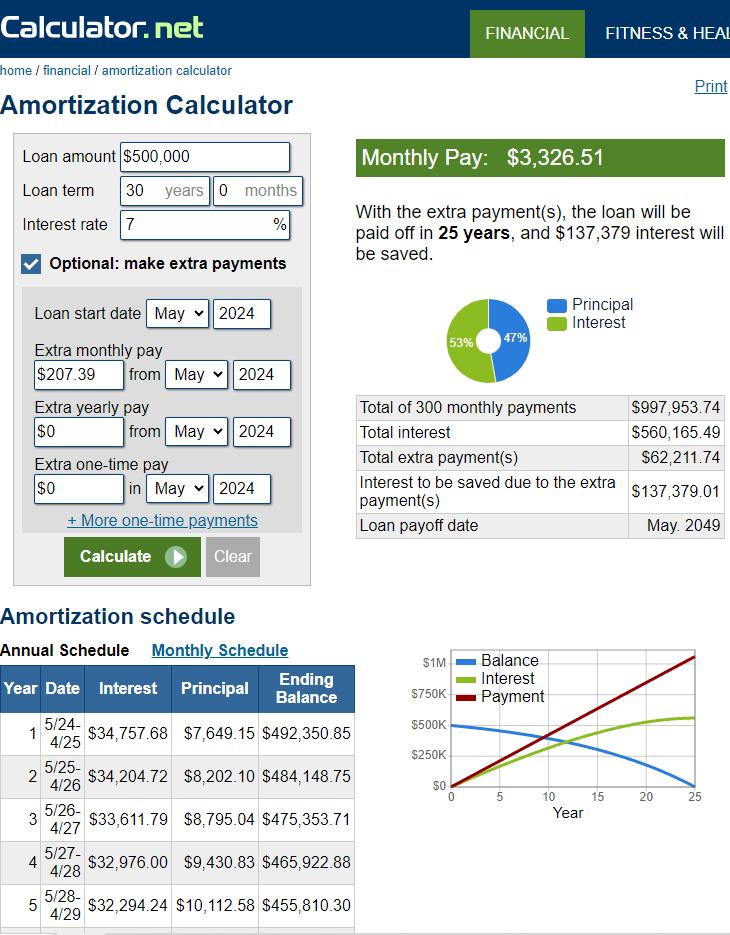

Go back to your calculator, remove the lump sum payment, and leave everything else the same, except the loan term. Change the loan term to 25 years instead of 30 years. Click calculate. Now look at just one number, the payment size. You’ll see it’s $3,533.90. Don’t worry about anything else, just note that number. Now reset to your original calculation of a 30 year term. You’ll see the payment size is back down to $3,326.51. Now get out your calculator and subtract $3,326.51 from $3,533.90. You’ll get $207.39. Go back to your “make extra payments” box and enter an “extra monthly pay” of $207.39. Click calculate.

As you can see, just by paying an extra $207 of principle every month, you’ll pay the loan off 5 years faster and save $137,379 in interest.

You’ll save a little less that way than the lump sum payment, because you’re not paying the principle down as much early in the loan. But paying an extra $200 a month is much easier for most people than accumulating thousands of dollars to make a large lump sum payment. A few hundred dollars is only about 6% of the size of this mortgage payment, so it’s really a small difference. And if you can’t afford to pay a few percent of your payment size extra each month, the mortgage is probably bigger than you can reasonably afford.

You can play around with these numbers in all kinds of ways. It’s a good way to help you think about your financial decisions, and the real impact they might have over time. Say for example, you’re considering buying a new grill for the backyard. You only grill a few times a month during the summer, and a replacement model of the basic charcoal grill you have now would be perfectly serviceable. It’s available for $119 on Amazon. But your brother-in-law just bought one of those Big Green Eggs and he keeps bragging about how amazing it is. They’re $1,950, but you can afford it, you just got a nice little bonus at work. So why not?

But before you get out the checkbook, let’s take a quick look at the mortgage calculator. Let’s see how much that extra $1,831 spent on a grill you don’t really need will actually cost you. Again, input your mortgage size, term, and interest rate, and add an extra one-time payment of $1,831.

Hopefully you’re still using that Big Green Egg in 30 years, because by that time, it will have cost you almost $13,000 in additional interest payments.

You can fill in the blank with your own discretionary purchases and see whether they’re really worth the cost. It’s just another little tool to help plan your financial decisions. It’s free to do, and can make a very significant difference in your financial well-being down the road. But almost no one takes advantage of the opportunity, so you’ll have a huge leg up on most people just by knowing this simple concept.

The Bottom Line

To take advantage of the opportunity to build wealth with a mortgage, there are only two simple rules.

Use a mortgage to buy a reasonably priced house that you couldn’t otherwise afford.

Take advantage of amortization to pay that mortgage off as fast as possible, so you pay as little interest as possible while still capturing the increase in price of the house.

If you already own a home, you can use the same concept. Take out a mortgage for whatever amount you’re comfortable with, and use the money to buy an asset that will increase in price with inflation. Choose your asset wisely, and don’t take on more debt than you can afford. But if you make good decisions, you can take advantage of the broken financial system, using this little mortgage cheat code to get the Cantillon effect on your side. The wealthy are doing it every day, so don’t miss the opportunity to lock in long-term, fixed rate debt and acquire hard assets. As the debt/credit fiat system implodes, the opportunity to do this will disappear. Take advantage of it while you can.

You're forgetting a teeny tiny concept called Opportunity Cost, which could invalidate the entire article. Not trying to be a d*ck, just something worth considering.

Comparing $30,000 one time payment to save $172,362 and pay the mortgage off in 25 years to investing that $30,000 in S&P 500 index assuming inflation adjusted average YoY return (6.37%) only nets $140,475. I was surprised and now finally convinced that paying off mortgage early especially with the high interest rates is worth it. However once you have an interest rate lower than 6.37% you net more money investing rather than paying off. (Maybe there are tax reasons paying mortgage off is better still even with a lower rate iif so please let me know)